The opportunities for furniture companies with manufacturing facilities in the United States are immense, but they must make greater investments to rebuild their domestic presence.

China has benefited from massive capital inflows from 1991 (the year it joined the WTO) until 2019 (pre-pandemic), which economists call net foreign investment.

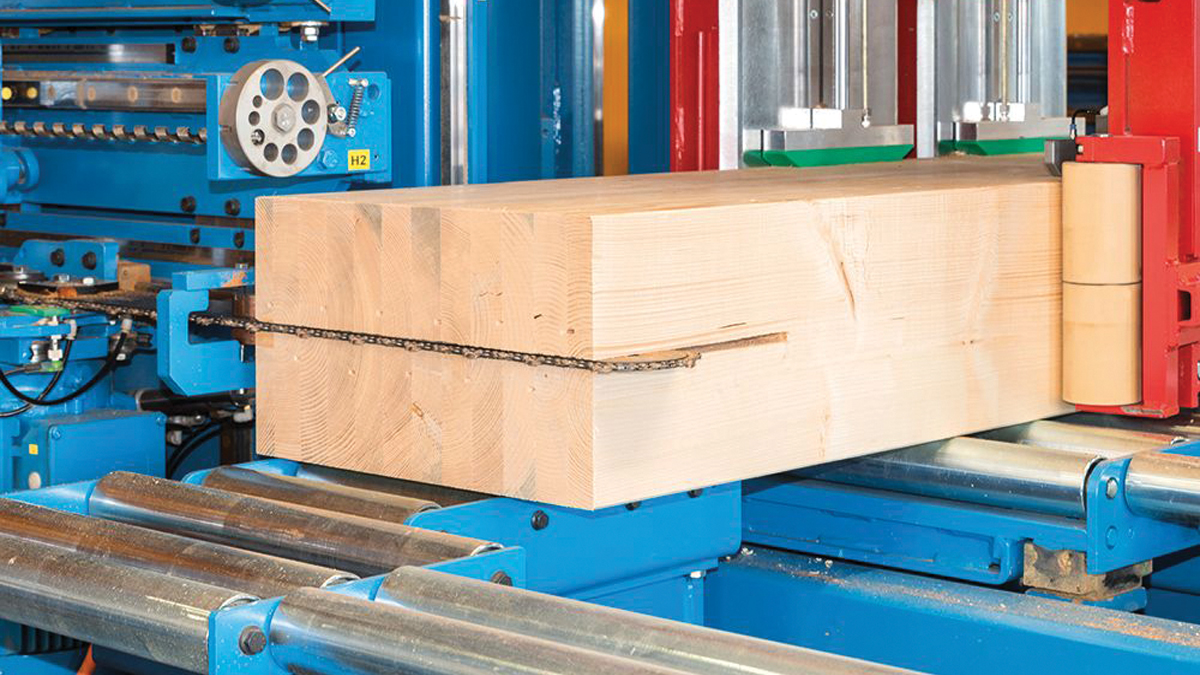

Expanding Space, Adding Machinery

For over two decades, China constructed or acquired an astonishing number of factories and production equipment. Thanks to bold investments, the country became the world’s largest furniture supplier, virtually dominating the global furniture supply chain. For many years, China was the top exporter of furniture to American consumers.

The U.S. doesn’t need to replicate China’s two-decade-long investment, but it will likely require several billion dollars to narrow the gap significantly. Thus, the first and most crucial step in bringing furniture manufacturing back to the U.S. demands substantial capital investment.

Gat Creek produces high-end solid wood furniture in a 140,000-square-foot factory in Appalachia, West Virginia. Recently, the company completed a $10 million expansion, increasing production space by 40% and investing in advanced machinery. The company employs about 215 workers and generates around $30 million in annual revenue.

Gat Creek was positioned as a “Made in America” brand from the start. When the company was bought 30 years ago, it was solely committed to domestic production. Industry insiders thought that this was foolish, as outsourcing to China or other countries clearly promised higher profit margins. However, today, people have rediscovered their appreciation for American manufacturing and what makes Gat Creek unique and better.

Understanding Consumers

The first advantage of domestic furniture manufacturers lies in their deep understanding of the local market. Then comes the speed of bringing durable goods to the market greater sustainability, and increased consumer trust. But the most significant differentiator is accountability. When a company lives and works in the same community, it bears responsibility for doing what is right for the environment, consumers, and employees.

These responsibilities pose additional challenges for American manufacturers competing with importers. They face higher healthcare expenses, stricter safety and environmental regulations, and elevated material costs.

Although labor costs have gradually decreased, they remain relatively high. Regarding materials, steel in the U.S. is significantly more expensive than almost anywhere else in the world. While lumber costs are competitive due to legal logging practices, many related materials lack this advantage.

As a result, U.S. furniture manufacturers tend to avoid the mid-range market segment, as this category is better suited to large-scale mass production. Instead, they target both the high-end and low-end segments. The high-end segment offers niche opportunities where American manufacturers have a competitive edge. Meanwhile, with scale, high automation, and smart production design, some domestic companies are effectively competing in the low-end segment.

The Trump administration’s previous tariffs on U.S. furniture imports shifted the supply chain from China to neighboring countries. With early policy moves in this re-election term, predicting how the supply chain will evolve next remains uncertain. But one thing is certain: the trend of reshoring manufacturing and bringing jobs back to the U.S. furniture industry is entirely feasible.

Gat Caperton – President of Gat Creek Furniture, U.S.

(FurnitureToday)